Earlier this year, the Economic Daily stated that "China adds certainty to the Southeast Asian economy."

The China-ASEAN Free Trade Area, established in 2010, now covers new fields like trade in goods, investment, digital economy, and green economy. Trade volume has surged from 443.6 billion RMB in 2013 to over 6.4 trillion RMB in 2023, accounting for 15.4% of China's total foreign trade.

Southeast Asia's own economic strength has also risen significantly, with a total GDP exceeding $3.6 trillion, making ASEAN the 5th largest economy in the world and the 3rd largest in Asia.

Chinese enterprises are rapidly expanding overseas, shifting focus from developed nations to developing ones, with Southeast Asia becoming a prime destination.

01. Economic Landscape: A Region on the Rise

By the end of 2022, Southeast Asia's total population reached 670 million, and GDP grew by 20% to $3.6 trillion. The per capita GDP of the 10 ASEAN countries rose to $5,395.

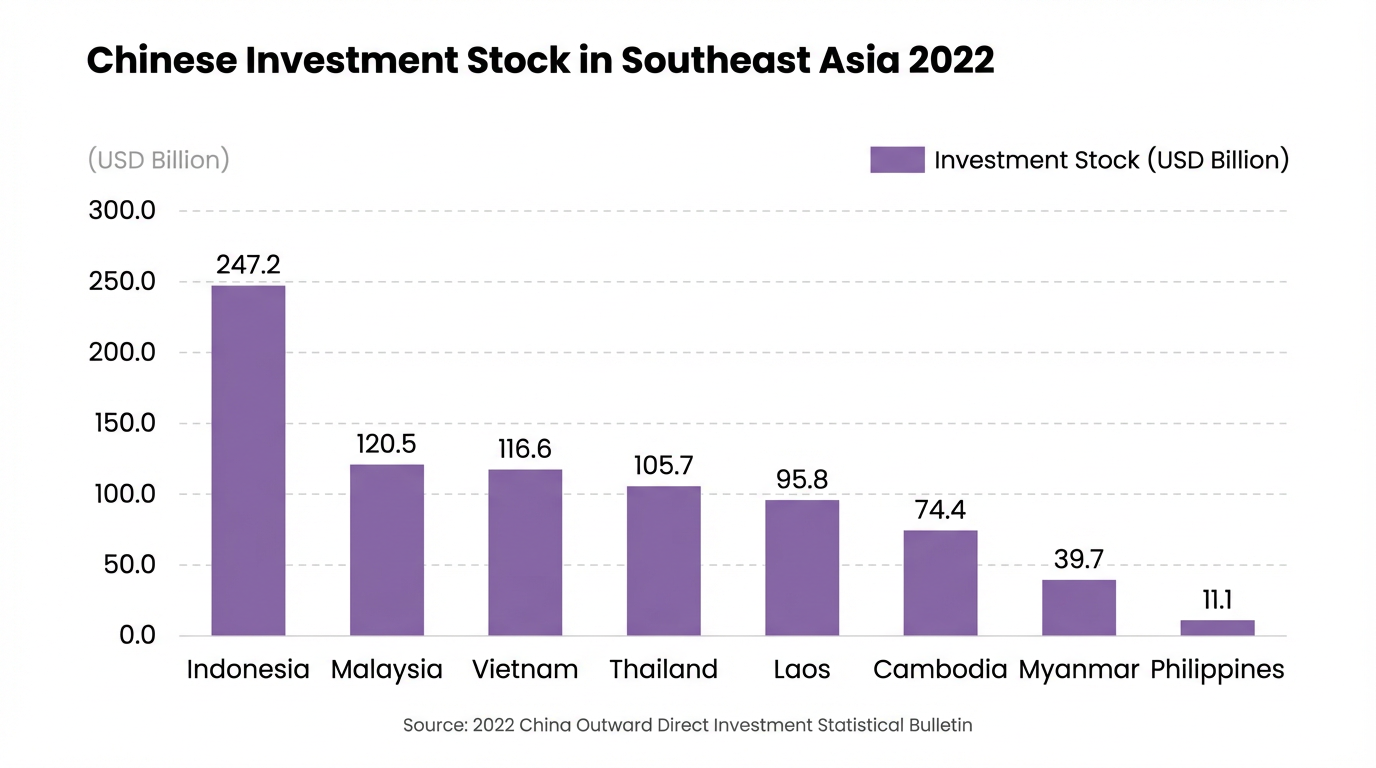

Since 2017, China's investment in ASEAN has outpaced investment in the EU and US. Indonesia received the largest stock of Chinese investment (nearly $25 billion), concentrated in Manufacturing (25%), ICT (18%), and Real Estate (17%).

Over 40% of Chinese enterprises plan to expand into Southeast Asia in the next three years, with Singapore, Thailand, and Malaysia as top destinations.

Country-by-Country Economic Snapshot (2023)

-

🇵🇭 Philippines (Top 1): Best economic performance with 5.6% GDP growth. Manufacturing is booming, though inflation remains high.

-

🇮🇩 Indonesia (Top 2): Driven by minerals. Manufacturing is expanding; consumer preference for e-payments is 67%.

-

🇻🇳 Vietnam (Top 2): GDP growth tied for 2nd. Strong in electronics. E-payment preference is high at 70%.

-

🇲🇾 Malaysia (Top 4): Service-oriented economy. Consumption growth is the highest in the region.

-

🇸🇬 Singapore (Top 5): Financial hub advantage keeps interest rates stable. E-payment preference is 66%.

-

🇹🇭 Thailand (Top 6): Facing manufacturing decline and deflation risks. E-payment preference is 60%.

Forecast: The region is expected to achieve 4.9% growth in 2024, with the Philippines, Cambodia, and Vietnam potentially exceeding 6%.

02. The Southeast Asian Gaming Market

Southeast Asia is the world's 4th largest gaming market.

-

Revenue: ~$1.6 billion in 2023.

-

Downloads: Reached 8.85 billion in 2022. Q1 2023 alone saw 2.1 billion downloads.

-

In-App Purchase (IAP): Revenue broke $2.7 billion in 2021.

Popular Game Genres by Country

-

Thailand: RPG, MOBA.

-

Indonesia: Shooting, Adventure, Competitive.

-

Philippines: Shooting, Action.

-

Malaysia & Vietnam: RPG, Strategy, Competitive.

-

Indonesia is the largest market by downloads (38% share), while Thailand, Singapore, and Malaysia lead in revenue.

Top Games Dominating the Region

-

Mobile Legends: Bang Bang (MOBA): The top-grossing game in Southeast Asia (2023 Q1), surpassing Free Fire. Huge in Philippines/Malaysia.

-

PUBG Mobile (Shooter): Extremely popular in Indonesia, Malaysia, and Thailand.

-

Dota 2 (MOBA): Strong PC player base in Singapore and Malaysia.

-

Garena Free Fire (Battle Royale): Fast-paced shooter loved in Indonesia, Thailand, and Singapore.

-

Ragnarok Online (MMORPG): A classic with a massive community in Thailand and Philippines.

03. Opportunities: Replicating the "China Miracle"

Southeast Asia offers massive potential:

-

Demographics: 680 million people, median age 29.8.

-

Internet Penetration: 75.6% average (Singapore/Malaysia >90%).

-

Copying Success: With a GDP per capita similar to China 10 years ago, Chinese game companies are successfully replicating their domestic strategies here.

Emerging Trend: Esports audiences are growing, and "Party/Sports" games are the fastest-growing categories in 2023.

04. Challenges for Game Exporters

-

Local Market Insights & Culture Religion and culture deeply influence business. Indonesia is Islamic, Thailand is Buddhist, and the Philippines is Christian. Logistics in island nations like Indonesia are costly. Political complexities (e.g., in Myanmar) add risk.

-

Regulatory Compliance From India's bans to rigorous app store takedowns, regulation is tightening around "Data Security." Compliance self-checks are crucial before entry.

-

Highly Fragmented Payment Landscape Southeast Asia has extreme currency diversity and payment fragmentation.

-

The Challenge: Users rely on diverse local wallets (e.g., GCash, Dana, MoMo) rather than credit cards.

-

The Solution: Companies need a resource-intensive solution to aggregate these. Waffo, for example, integrates 70+ currencies and 300+ payment methods across 50+ emerging markets, holding PCI DSS and Hong Kong MSO licences.

-

Lack of Ecosystem Partners Deploying globally is complex. Finding a one-stop partner for marketing, payments, and operations is difficult but essential for efficiency.

-

Technical Infrastructure Talent There is a shortage of global deployment and operations talent. However, Chinese cloud vendors (AliCloud, Tencent Cloud) are expanding rapidly in the region to support this technical infrastructure.

Conclusion In a changing international landscape, game companies must look beyond simple market expansion. The real challenge—and opportunity—lies in building a sustainable, localised strategy that integrates advanced resources, talent, and compliant payment infrastructure like Waffo to win the long game in Southeast Asia.