Compliance with local tax regulations is a critical, non-negotiable aspect for any global enterprise expanding overseas. To support Chinese businesses in their global journey, we are launching the "Waffo Tax Talk" column. This series will decode the tax systems and risk alerts of key international markets. First stop: Indonesia.

01. Economic Overview

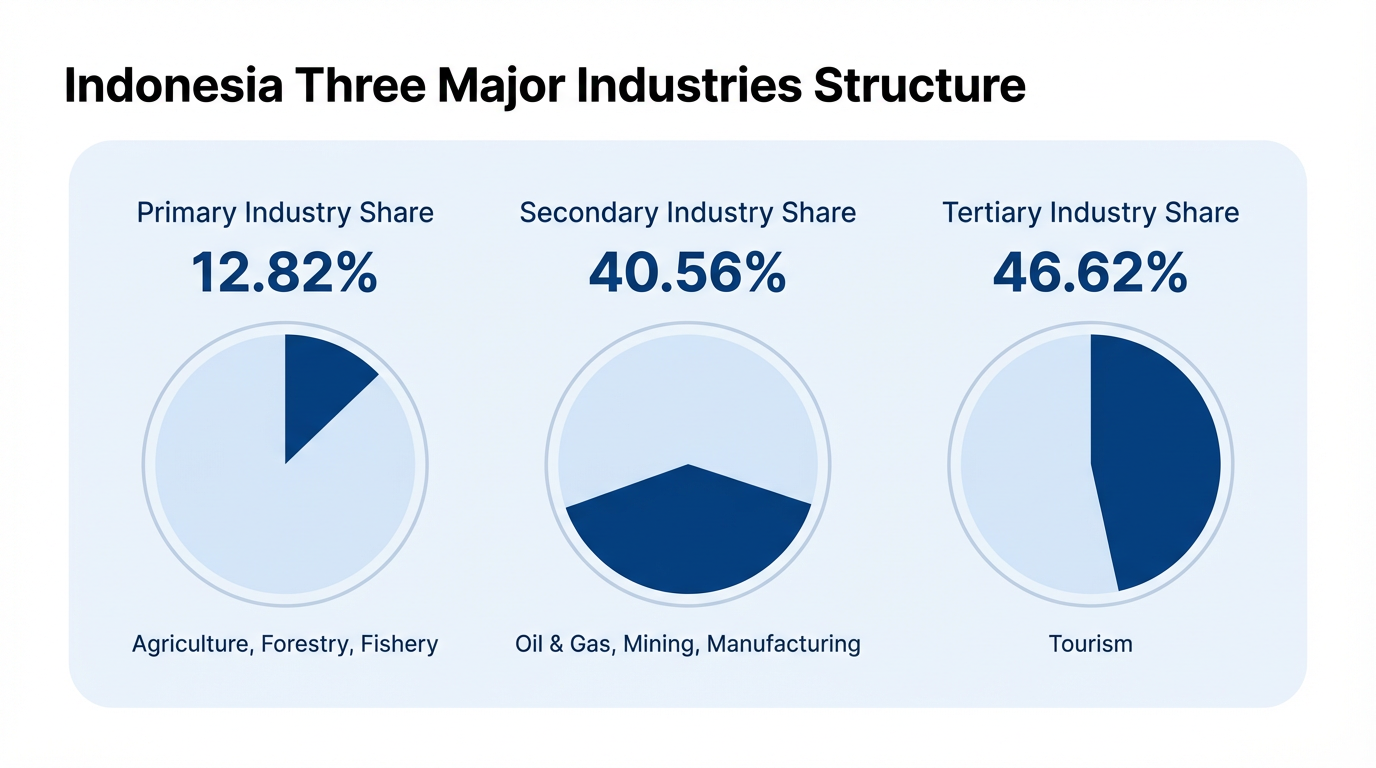

Indonesia, ASEAN's largest economy, maintains robust growth driven by domestic consumption.

-

Structure: A balanced economy with strong agriculture, industry, and service sectors.

-

Outlook: Positive macroeconomic indicators and unique comparative advantages continue to attract foreign investment.

(For a deeper dive into the market, read our previous report: "Indonesia Payment Market Overview")

02. Key Taxes in Indonesia

Indonesia operates a two-tier tax system (Central and Regional). While legislation is centralized, local governments have specific regulatory powers.

1. Corporate Income Tax (CIT)

A. Resident Companies Entities established or registered in Indonesia (including Permanent Establishments).

-

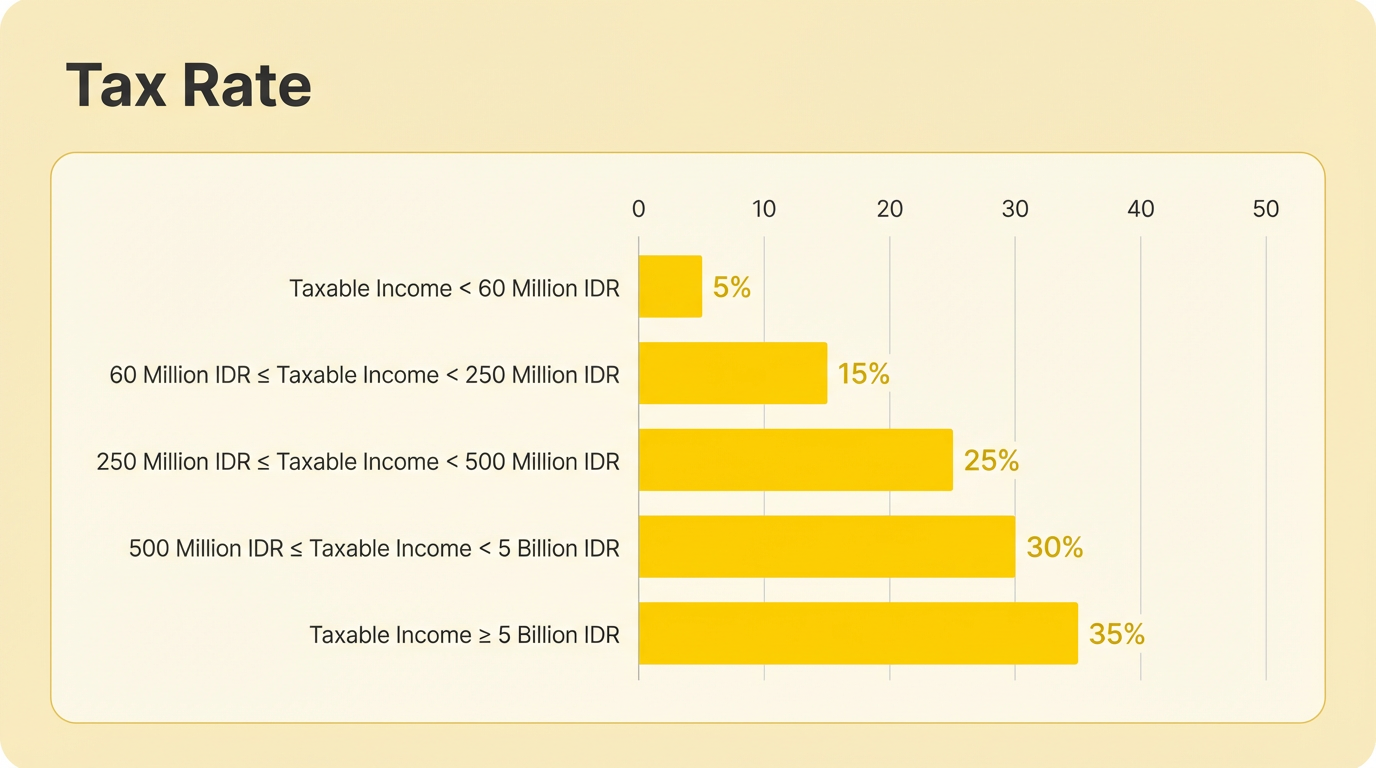

Standard Rate: 22%.

-

SME Incentives:

Small and Medium Enterprises (SMEs) may enjoy a 50% tax reduction.

Micro-enterprises with gross turnover below IDR 4.8 billion may pay a final tax of 0.5% on turnover for the first 3 years.

B. Tax Incentives (Tax Holiday)

-

Exemption: Companies meeting specific criteria can enjoy a 50% or 100% CIT exemption for 5 to 20 years, depending on the investment amount.

-

Post-Holiday: A 25% or 50% reduction is available for 2 years after the holiday period expires.

C. Non-Resident Companies Taxed only on income derived from Indonesia, at the same rate as resident companies (unless a tax treaty applies).

2. Value Added Tax (VAT)

For digital entertainment and SaaS companies, this is critical.

-

Standard Rate: 11% (adjustable between 5% and 15%).

-

VAT Collector: Foreign digital service providers must collect VAT if:

Transaction value exceeds IDR 600 million (~$38k USD) annually or IDR 50 million monthly.

Traffic/access exceeds 12,000 users annually or 1,000 users monthly.

-

Compliance: You must issue VAT-inclusive invoices containing your name, address, tax ID (NPWP), and tax breakdown. Failure to do so can lead to penalties.

-

Exemptions:

Mining/drilling products directly from the source.

Basic necessities, medical services, financial services, and education.

Low-cost housing.

3. Other Key Taxes

-

Stamp Duty: A fixed rate of IDR 10,000 on specific documents (agreements, notarial deeds, high-value securities).

-

Customs Duty: Import duties range from 0% to 150% (CIF basis). Incentives are available for government projects, Special Economic Zones (KEK), and Free Trade Zones (FTZ).

03. Risk Management & Compliance

1. Reporting Risks

-

Entity Type: Foreign investors must establish a PT PMA (Foreign Investment Limited Liability Company).

-

Obligations: PMAs are tax residents and must file monthly and annual returns for CIT, VAT, and Withholding Tax (WHT). Investment plans must also be reported.

2. Filing Deadlines

-

Monthly WHT: Pay by the 10th, file by the 20th of the following month.

-

Monthly VAT: Pay and file by the end of the following month.

-

Annual CIT: File by the end of the 4th month after the tax year ends.

3. Audit Risks

Indonesia uses a Self-Assessment System. However, tax authorities (DGT) can audit returns.

-

Trigger: Refund applications almost always trigger an audit.

-

Scope: Audits can cover all taxes for a specific period or year.

4. Tax Treaty Benefits

Many companies miss out on lower withholding tax rates under Double Tax Agreements (DTA) due to:

-

Lack of knowledge about the China-Indonesia tax treaty.

-

Failure to obtain a Certificate of Domicile (COD).

-

Poor communication with local accounting firms.

Conclusion: Plan Before You Act

Before entering Indonesia, conduct thorough tax due diligence.

-

Pre-entry: Understand the tax implications of your business model.

-

Operation: Ensure timely and accurate filing to avoid penalties.

-

Rights: Leverage tax incentives and treaty benefits to optimize your tax position.