Compliance with local tax regulations is a critical, non-negotiable aspect for any global enterprise expanding overseas. Following our previous guide on Indonesia, the "Waffo Tax Talk" column continues to decode the tax systems and risk alerts of key international markets. This edition focuses on Thailand.

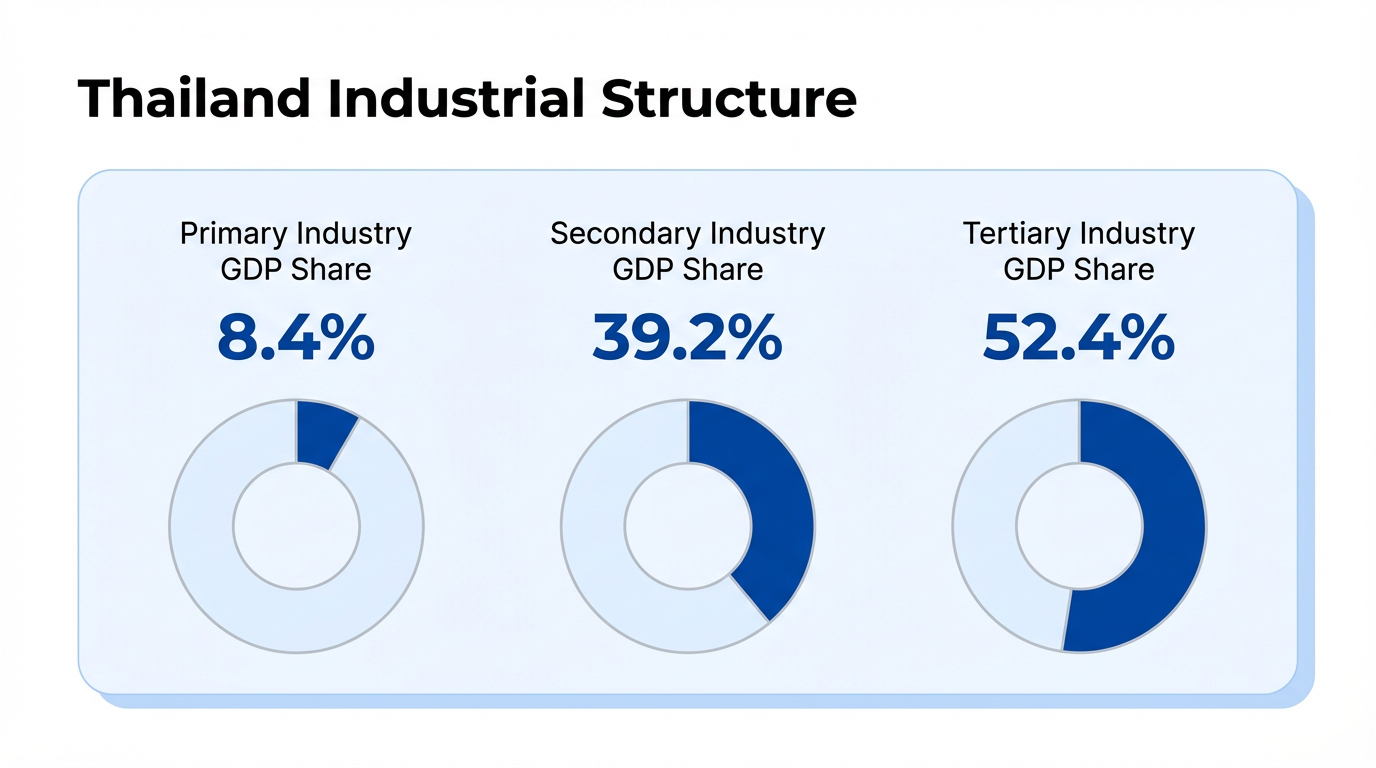

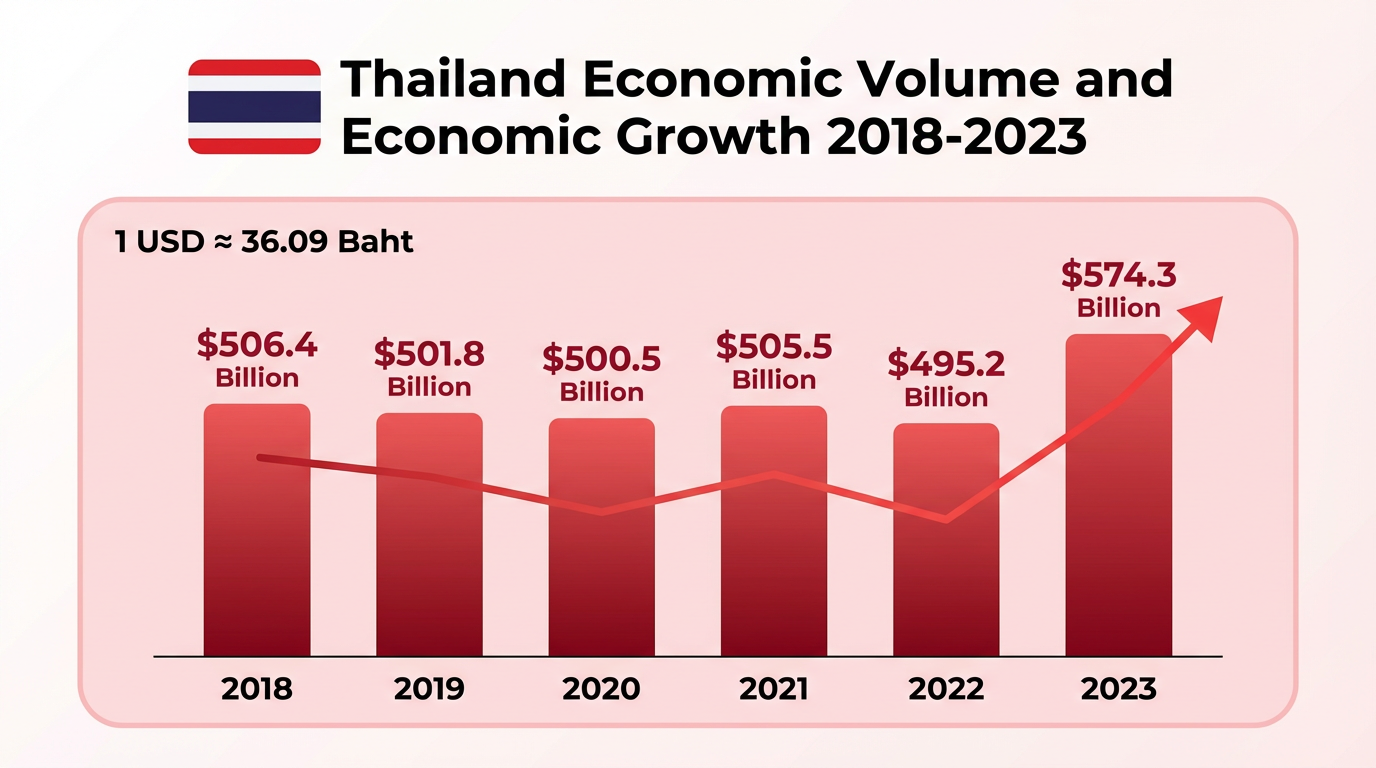

01. Economic Overview

Despite global fluctuations, Thailand remains a powerhouse in Southeast Asia.

- Key Industries: Tourism, industry, and agriculture form the backbone of the economy.

- Manufacturing Hub: Thailand is the automotive manufacturing centre of Southeast Asia and ASEAN's largest automotive market. The electronics industry is also growing rapidly.

(For a deeper dive into the market, read our previous report: "Thailand Payment Market Overview")

02. The Tax System & Legal Framework

1. Legal Framework

The foundation of Thailand's tax system is the Revenue Code (1938), which governs Corporate Income Tax (CIT), Personal Income Tax, VAT, Specific Business Tax, and Stamp Duty.

- Authority: The Ministry of Finance and the Cabinet can amend the code via Royal Decrees to adapt to economic needs.

2. Administration

The Revenue Department administers tax collection. Thailand follows a Self-Assessment System, where taxpayers are legally obligated to declare income and pay taxes. Tax evasion carries severe penalties.

3. "Thailand Plus" Incentives

To attract investment, Thailand launched the "Thailand Plus" package in 2019.

-

Eastern Economic Corridor (EEC): Investments in the EEC can enjoy tax holidays or reductions for up to 13 years.

-

Deductions: Additional deductions are available for hiring high-skilled STEM talent, employee training, and investing in automation/robotics.

4. Electronic Services Tax

Since September 1, 2021, foreign electronic service providers must collect 7% VAT on services provided to non-VAT registered customers in Thailand. This creates a level playing field for local and foreign operators.

03. Key Taxes in Thailand

1. Corporate Income Tax (CIT)

A. Resident Companies Entities incorporated under Thai law (e.g., Limited Companies, Public Limited Companies).

-

Standard Rate: 20% on net profit.

-

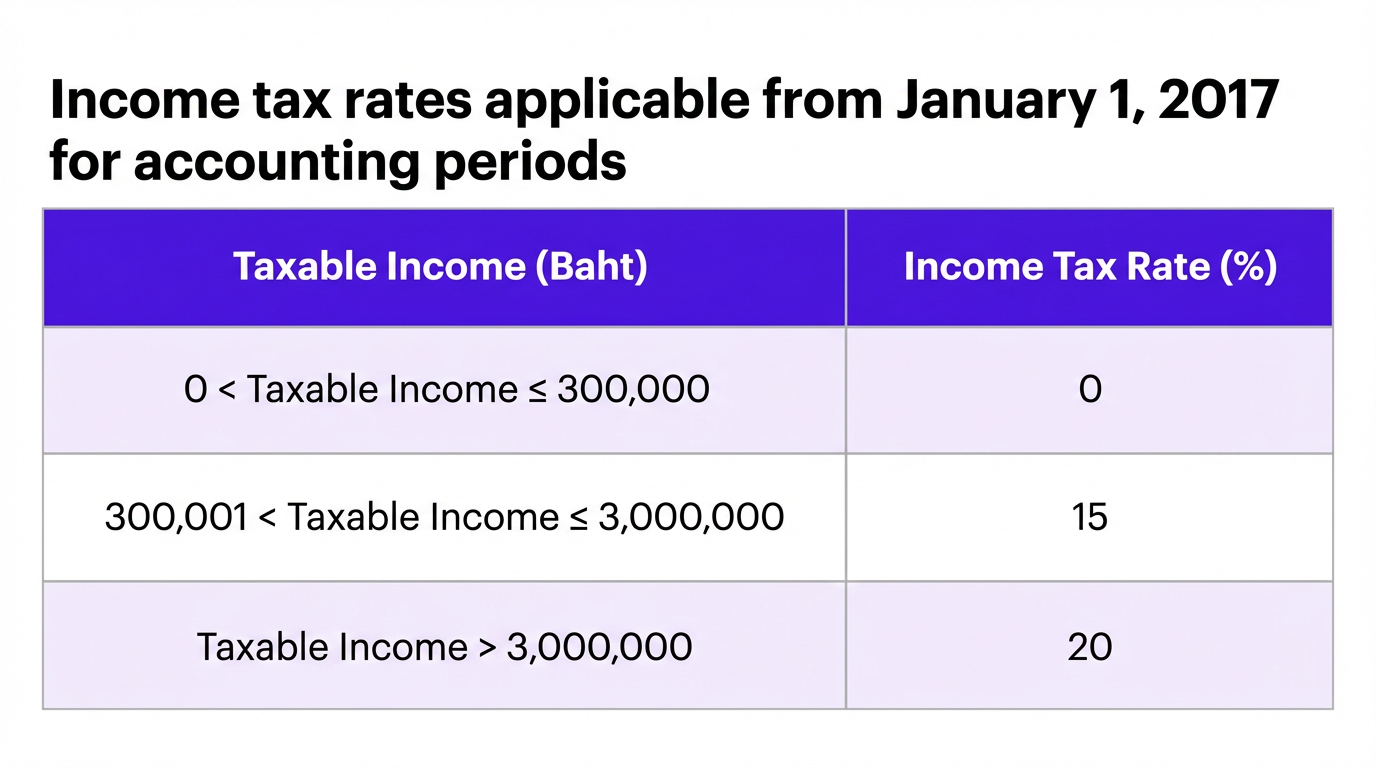

SME Incentives:

Paid-up capital ≤ 5 million THB AND income ≤ 30 million THB.

Tax Rate: Progressive rates (0% for first 300k, 15% for 300k-3m, 20% for >3m).

- Withholding Tax (WHT):

10% on dividends remitted abroad.

15% on other income (e.g., royalties, interest) remitted abroad.

B. Non-Resident Companies Companies not incorporated in Thailand but deriving income from Thailand.

Carrying on Business in Thailand: Taxed on net profit at 20% (same as resident).

Not Carrying on Business in Thailand: Taxed on gross income paid from or in Thailand (usually via WHT at 15% or 10%).

C. Tax Incentives (BOI) The Board of Investment (BOI) offers generous incentives:

- Tax Holidays: CIT exemption for up to 13 years for eligible activities.

International Business Centre (IBC): Reduced CIT rates of 8%, 5%, or 3% for 15 years, depending on expenditure in Thailand (60m, 300m, or 600m THB).

2. Value Added Tax (VAT)

A. Scope VAT applies to the sale of goods, provision of services, and imports.

-

Threshold: Compulsory registration for businesses with annual turnover exceeding 1.8 million THB.

-

Digital Services: Foreign digital service providers must register if income from Thai non-VAT registrants exceeds 1.8 million THB/year.

B. Rate

-

Standard Rate: Reduced to 7% (from statutory 10%) to support the economy.

-

Zero Rate (0%): Applies to exports of goods/services, international transport, and sales to UN agencies/embassies.

C. Exemptions

Small businesses (turnover < 1.8m THB).

Sales of agricultural products, newspapers, and educational/medical services.

(Caption: Key tax rates in Thailand: CIT at 20% and VAT reduced to 7%.)

3. Customs Duty

Duties range from 0% to 80% based on the Harmonized System (HS) code.

- Exemptions: Available for Free Trade Zones (FTZ), Bonded Warehouses, and BOI-promoted projects.

04. Risk Management & Compliance

1. Information Reporting

Chinese resident enterprises must report their shareholdings in Thai companies to Chinese tax authorities if ownership reaches or exceeds 10%.

2. Transfer Pricing (TP) Risks

The Revenue Department scrutinizes related-party transactions. High-risk indicators include:

-

Significant related-party transactions.

-

Continuous losses for >2 years.

-

Lower profit margins compared to competitors.

-

Payment of management fees or royalties to related parties.

3. Tax Treaty Benefits

Enterprises often fail to claim benefits under the China-Thailand Double Taxation Agreement (DTA) due to:

Lack of proper documentation (e.g., Certificate of Residence).

Failure to apply for foreign tax credits in China to avoid double taxation.

Conclusion: Plan Before You Act

Expanding into Thailand requires a clear understanding of its tax landscape.

-

Due Diligence: Understand the tax implications before setting up.

-

Compliance: Adhere to filing deadlines and transfer pricing rules.

-

Optimization: Leverage BOI incentives and DTA benefits to maximize efficiency.