Compliance with local tax regulations is a critical, non-negotiable aspect for any global enterprise expanding overseas. Following our previous guides on Indonesia and Thailand, the "Waffo Tax Talk" column continues to decode the tax systems and risk alerts of key international markets. This edition focuses on Vietnam.

01. Economic Overview

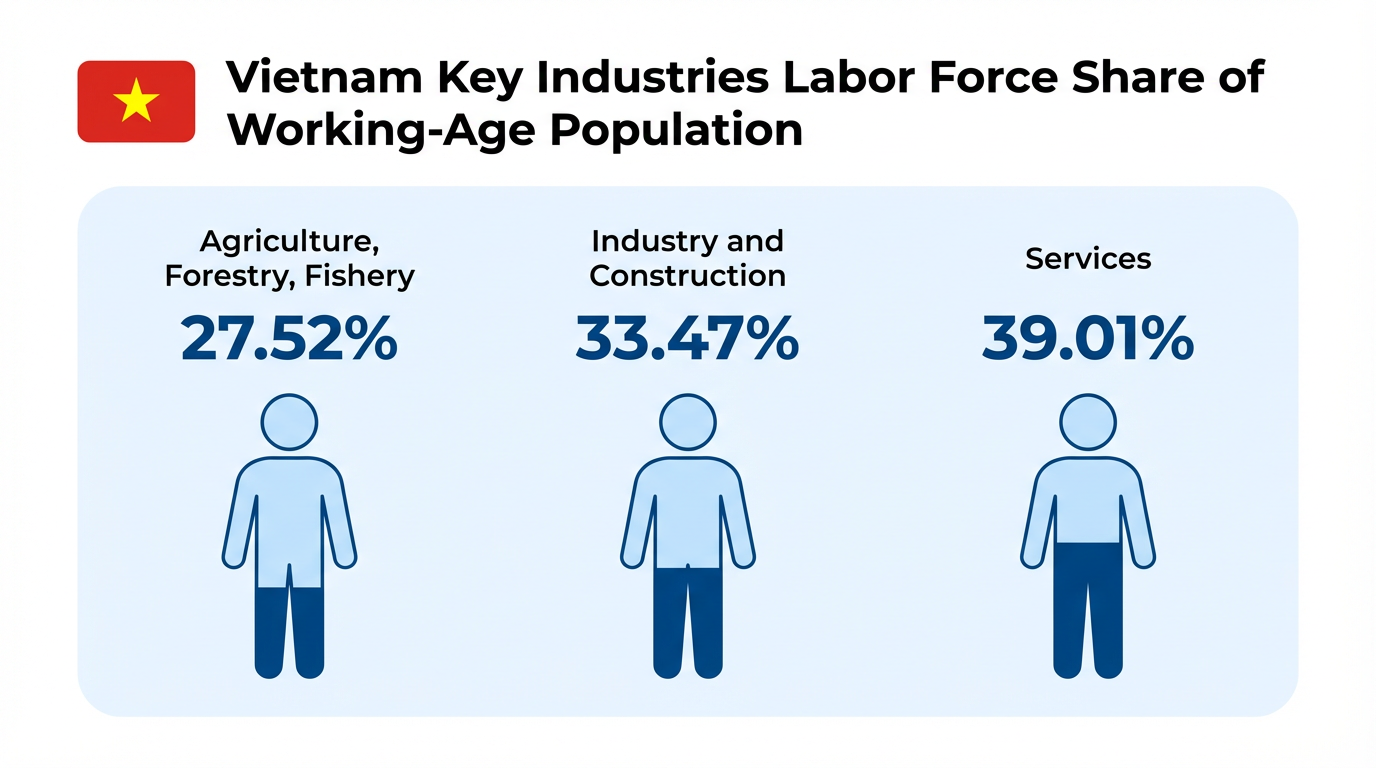

Vietnam has transformed from a traditional agricultural nation into a booming market economy.

-

Growth: From 2002 to 2021, GDP per capita increased by 3.6 times. In 2023, GDP reached $430 billion.

-

Key Industries: Metallurgy, electronics, green energy, and logistics are prioritized for mid-to-long-term development.

(For a deeper dive into the market, read our previous report: "Vietnam Payment Market Overview")

02. The Tax System & Legal Framework

1. Legal Framework

Taxation power is centralized. Key laws include the Law on Tax Administration, Law on Corporate Income Tax (CIT), Law on Value Added Tax (VAT), and Law on Personal Income Tax (PIT).

2. Reform Trends

Vietnam is actively simplifying tax procedures and digitizing administration to improve the business environment. New regulations target e-commerce and transfer pricing to ensure fair competition between digital and physical businesses.

03. Key Taxes in Vietnam

1. Corporate Income Tax (CIT)

A. Resident Enterprises Entities established under Vietnamese law.

-

Scope: Taxed on worldwide income.

-

Taxable Income: Includes operating income, service income, and other income (e.g., capital gains, IP royalties, asset transfers).

-

Standard Rate: 20% (effective from Jan 1, 2016).

B. Non-Resident Enterprises Entities without a permanent establishment in Vietnam but deriving income from Vietnam.

-

Withholding Tax: Vietnamese parties paying income to foreign entities must withhold tax (Foreign Contractor Tax).

-

Rate: Generally 20% for CIT if a permanent establishment exists.

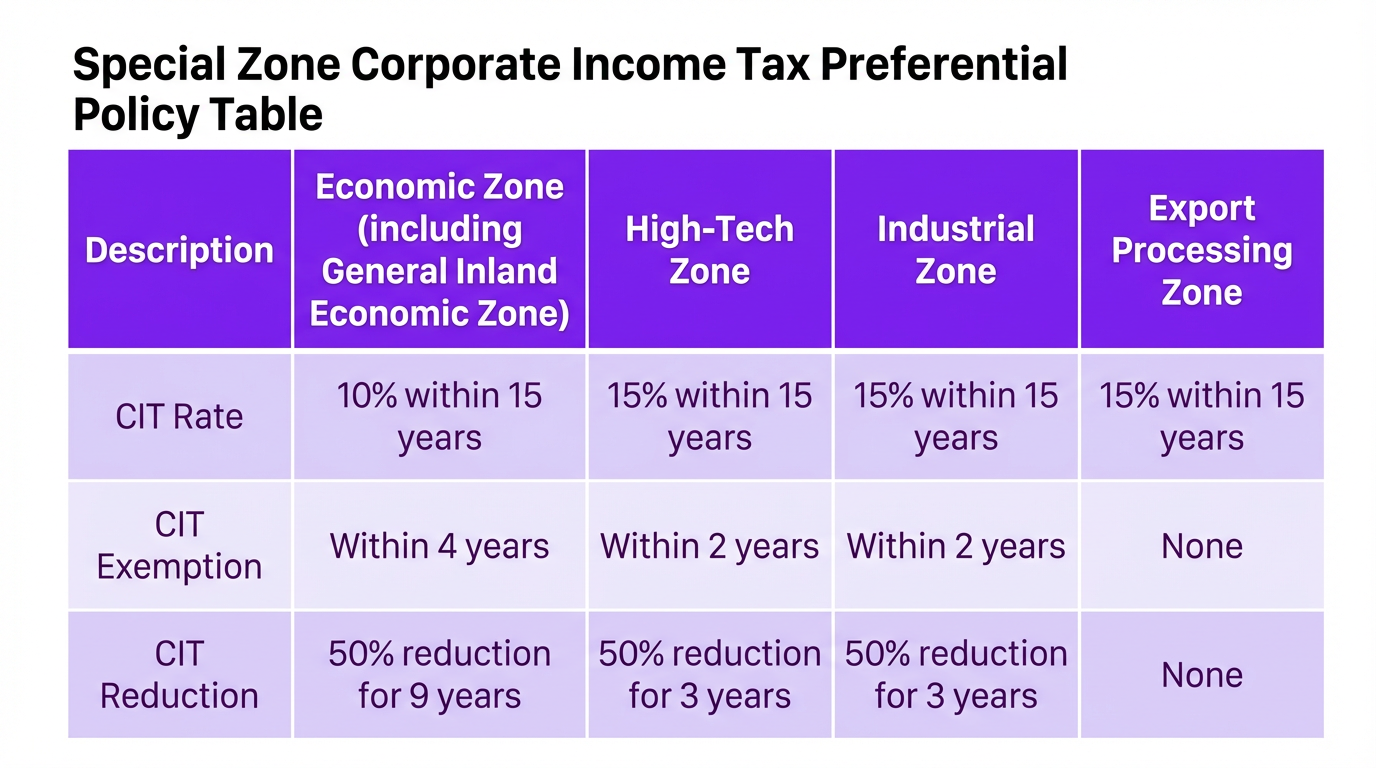

C. Tax Incentives Vietnam operates a self-assessment system for incentives. Companies determine their eligibility, calculate reductions, and declare them at year-end.

- Risk: If tax authorities later find the company ineligible, they will demand back taxes, interest, and penalties (1-5 times the unpaid amount).

2. Value Added Tax (VAT)

A. Digital Services Tax For digital entertainment and SaaS companies, Vietnam's VAT rules are strict.

Registration: Mandatory for all foreign digital service providers. Unlike Indonesia (threshold-based), Vietnam requires registration from the first transaction.

B. Scope VAT applies to goods and services used for production, trading, and consumption in Vietnam.

C. Rates

-

Standard Rate: 10% (applicable to most digital services).

-

Reduced Rates: 5% (e.g., clean water, teaching aids) and 0% (exports).

D. Incentives

-

Exemptions: Software products, medical services, and derivative financial services.

-

Non-Tariff Zones: Goods/services traded within export processing zones are exempt.

3. Import & Export Duties

Duties are determined by the Ministry of Finance based on HS codes.

-

Common Rate: Preferential Rate × 150%.

-

Calculation: Duty = CIF Value × Rate.

-

VAT on Imports: (CIF Value + Import Duty) × VAT Rate.

-

Preference: Utilizing Certificate of Origin (C/O) can reduce duties to 0% under trade agreements (e.g., ACFTA).

04. Risk Management & Compliance

1. Information Reporting

Foreign investors must strictly follow the "Application - Registration - Publication" process. All data provided to tax authorities must be complete, accurate, and timely.

2. Declaration Risks

-

Errors: Incorrect declarations leading to tax underpayment will face penalties and interest.

-

Voluntary Correction: If a taxpayer corrects errors before a tax audit notification, penalties may be waived, leaving only the tax and interest to be paid.

3. Transfer Pricing (TP) Risks

Vietnam is aggressively targeting transfer pricing.

-

Documentation: Related-party transactions must be documented and justified as arm's length.

-

Burden of Proof: Companies have 90 days to prove compliance if challenged by tax authorities.

4. Double Taxation

Cross-border businesses face the risk of double taxation. Leveraging Double Tax Agreements (DTA) is crucial to minimize tax burden, but requires careful planning and documentation.

Conclusion: Plan Before You Act

Vietnam's self-assessment system places the burden of compliance on the taxpayer.

-

Due Diligence: Understand your obligations before entering the market.

-

Digital Tax: Ensure you register for VAT if you sell digital services.

-

Incentives: Self-assess carefully to avoid future penalties.